Software and AI: Separating Fear from Fundamentals

- David Wrigley, CFA®, CAIA®

- Feb 19

- 7 min read

Updated: Mar 3

Overview:

What happens when the most disruptive technological force in a generation (AI) turns its sights on the very industry that built it? That's the question confronting software investors today. In recent months, following exceptional returns over the last decade, the market is assuming the software industry will be among AI’s biggest casualties. The view has quickly pivoted from “software is eating the world” to “AI is eating all software.”

At the center of the debate is whether software can survive in a world where AI “vibecoding” tools can build anything the mind can conceive in a weekend, with very little technical expertise and near-zero cost. We think the answer is yes, but with a strong caveat: survival will not be universal. Companies that embrace AI as a tool for reinvention and transformation will thrive. Those that don't will languish, much like newspapers that ignored the internet, retailers that dismissed e-commerce, and taxi companies that underestimated ridesharing.

The AI Era:

The AI era is here, and its impact is exploding. LLMs like ChatGPT, Gemini, and Claude have become nouns and are part of many people’s everyday routine. These models learn patterns from massive datasets and use them to generate new text, images, audio, and code. The accelerated speed of code writing has been one of the largest breakthroughs.

Each new LLM version is exponentially more powerful, and the rate at which they are improving is staggering. The notion that AI can build the next AI is now emerging. The next frontier is agentic AI, where models move beyond generating content to autonomously making decisions and completing complex tasks. So far, no major AI lab has created a durable advantage, and we’ve seen some leapfrogging across reasoning, speed, and task-specific performance from version to version. The competitive moats around AI tools remain unclear, and the winner-take-most dynamic is far from settled.

AI is already reshaping the economy, enabling faster and better decision making, transforming operational workflows, and allowing companies to extract more output from their existing workforce. And that comes at a time when, according to Blackstone, 61% of enterprises are still in early AI testing or proof-of-concept phases.¹ We believe AI will become the most revolutionary productivity driver for the global economy since the advent of electricity or the automobile. The speed of this transformation is what has the market on edge.

Shoot First, Ask Questions Later:

As an example of how quickly AI is evolving, Anthropic and other labs recently released powerful new productivity tools geared toward helping corporations. These plugins marked a clear shift from AI-as-chatbot to AI-as-enterprise-worker, igniting a fierce selloff of many stocks tied to knowledge workers that are viewed as vulnerable. Industries spanning software, accounting, consulting, law, insurance, finance, design, and customer service all took it on the chin in recent weeks.

Last week, the major real estate brokers and pureplay office REITs were down 15% given a fresh wave of concerns surrounding long-term office space demand. On February 9, insurance brokers were hammered 10-15% when OpenAI announced an AI insurance tool embedded in ChatGPT. The freight and logistics names were clobbered when a penny stock with a $20MM market cap (MIME) announced that its customers are seeing surging productivity gains from its AI freight tool, causing several $20BN+ market cap companies to shed 10% of their value. It has felt like the meme of the grim reaper going from door to door seeking destruction.

Software’s vulnerability has also been front and center. Given the perception that AI is going from augmenting software to being a direct competitor and potential replacement, many software stocks are now down 15-35% YTD. The iShares Software ETF (IGV) is in a bear market, down 22% YTD through last Friday. Trillions of dollars of market cap have been erased. Some are drawing parallels to the DeepSeek shock from January 2025, which triggered a sharp but short-lived selloff in AI-centric U.S. tech stocks on disruption fears.

Valuation Compression:

Software has historically traded at much higher valuations than the overall market given its recurring revenues, high growth rates, and great margins. Given the AI threat, the perception of the group’s safety has eroded. The market is concluding that the durability of software companies’ growth rates and the predictability of their margins and terminal cash flows are in question. This lower confidence has ignited a fierce valuation reset. From a valuation perspective, the software sector has experienced a dramatic 33% de-rating since October 2025, despite forward earnings estimates having gone up 5% since then.

Shown below by Morgan Stanley, this valuation compression is similar to prior periods of peak panic and uncertainty.² The group’s valuation of 4.4x EV/Sales is the lowest since 2014-2016, when the emergence of cloud computing caused a similar level of fear that software was being disrupted. That was also a "shoot first, ask questions later" environment. Cloud computing, of course, turned out to be a positive transformation for software, not an extinction. We see a similar dynamic playing out today with select companies.

Software Isn’t Dead, It’s Evolving:

The irony of this software dislocation is that AI is actually creating an explosion of new software demand, unlocking vast unmet need across every facet of our work and personal lives. The addressable market for software is expanding, not contracting. Despite that growth, the market is concluding that the ease and low cost of building software will erode incumbents' pricing power. The logic is that if AI enables fewer workers to accomplish the same output, that means fewer subscriptions and margin pressure for some. Others could see revenue gradually erode as AI agents replace humans in workflows. There will absolutely be software casualties.

But the narrative that the majority of enterprises will uproot core systems and either “vibecode” their own proprietary stack or replace them with newly built systems is farfetched. In many cases, the switching costs are substantial, execution risk is high, and there is deep data lock-in. Many firms operate with multi-layered integrations across internal systems and external data providers, and each additional integration increases operational fragility and cybersecurity risk. This level of retraining, data migration, and workflow disruption might not be a big deal for simple small businesses; but for management teams of large enterprises, it's a nonstarter.

Further, the market is giving incumbent software too little credit for their ability to capture AI-driven value. As we've seen with new entrants, agentic AI capabilities that surface new insights can command premium pricing, meaning simple AI features may be able to increase revenue to offset losses elsewhere. Also, in a world where every startup can spin up new software tools, the landscape gets increasingly noisy. That confusion could actually entrench companies in the established names they trust.

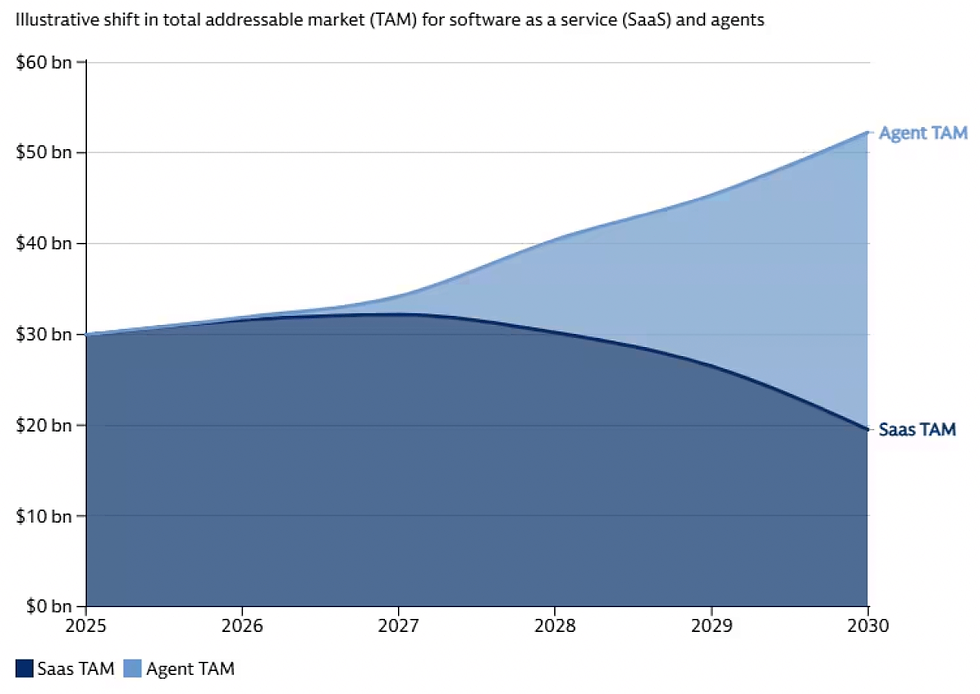

We believe most large enterprises will prioritize agentic AI add-ons and incremental feature improvements rather than full-scale rebuilds. As the overall software market continues to grow, agentic AI will capture a greater amount of the profit pool. Goldman Sachs shows below how the profit pool of customer service software may evolve.³ Though customer service is a narrow segment of the ~$750BN application software TAM, it’s remarkable that agentic AI could capture ~60% of that market by 2030.

Software has reinvented itself before, and we think the companies with established moats can widen and deepen them using AI. As Darwin would remind us, it is not the strongest that survives, nor the smartest, nor the best resourced; it is the one most responsive to change. Companies that integrate AI into their platforms can survive and become even more dominant. Companies that don't will find themselves on the wrong side of the profit pool shift, earning spots alongside Blockbuster and Sears in capitalism's hall of shame. The question for investors is how to tell the difference.

Separating Winners from Losers:

What the market is getting wrong is the lack of differentiation from software stock to software stock. This indiscriminate selling is a classic "throw the baby out with the bathwater" event. AI will result in some software companies not just surviving but thriving, while obliterating others. The key is identifying the companies treating this disruption as a catalyst for reinvention and avoiding the ones clinging to legacy business models.

In our view, the software winners will be those with the highest switching costs given their entrenched, mission-critical workflows and deep integrations, those that own their data, those with the greatest network effects, and those with multi-layered platforms that enable agentic AI to be efficiently incorporated. Trust and adaptability in the face of swift evolution will also be critical. Companies lacking those attributes will die slow, painful deaths.

We believe the current selloff is creating opportunities in select high-quality software names where the market has conflated short-term uncertainty with long-term impairment. Cybersecurity is a category where trust is non-negotiable, switching costs are high, and cyber threats accelerate and grow more complex with the proliferation of AI. Other integrated software platforms are embedded so deeply across enterprise workflows that the sheer complexity of extracting them makes them defensible. The firms that combine AI capabilities with proprietary data, integrated workflows, and domain expertise are positioned to become ever bigger than before.

Summary:

The market's indiscriminate repricing of software stocks reflects a level of fear that, in our view, is not matched by the fundamentals. Yes, AI is reshaping the competitive landscape and there will be real casualties. But the current selloff mirrors past episodes of broad-based tech panics that created compelling opportunities in the companies best positioned to adapt. Software isn't dying; it's entering its next chapter.

We are not dismissing the risks. AI is moving fast, and companies that fail to evolve will be left behind. But the winners with deep integration, entrenched data, high switching costs, and the ability to embed agentic AI into their platforms are being unfairly punished alongside the losers. We believe the companies that lead this reinvention will emerge stronger than ever.

David Wrigley

Chief Investment Officer

Blackstone’s 3Q25 CEO Survey, as of October 9, 2025

Morgan Stanley Research, as of February 8, 2026

Goldman Sachs, as of July 3, 2025

The information contained herein is the opinion of the author as of the date the market update was written and is subject to change without notice as markets change, and new information is available. While Diversify utilizes sources deemed to be reliable, we have not independently verified the content. Investors should carefully consider any changes based on this market commentary and discuss their individual circumstances with their trusted advisors. Past performance is not indicative of future results. This communication is for informational purposes only and should not be construed as investment advice or a recommendation.