The Iran Conflict’s Chain Reaction

- David Wrigley, CFA®, CAIA®

- Apr 6

- 8 min read

Overview:

In our March 5th piece, we summarized the initial implications of the U.S.-Israel strikes on Iran and the effective closure of the Strait of Hormuz. We discussed the tail risk of oil moving from pre-war levels (mid-$60s for WTI) to over $100 per barrel due to largescale supply shocks and the potential that energy infrastructure would be targeted. This has become a reality.

Five weeks later, the conflict has lasted longer than many expected. The Strait remains effectively closed, which has resulted in the largest energy supply disruption on record. Brent and WTI are both hovering around $110 per barrel, global interest rates have climbed due to inflationary concerns, and broad equity indices are down 5-10% from their February highs. There have been de-escalation attempts, but none have gained traction. The economic and market implications we flagged as possibilities are now materializing.

This piece picks up where the prior one left off, with a focus on what we think matters most right now for financial markets: the connection between elevated energy prices and upward pressure on inflation, the broad repricing of interest rates, the direction of global monetary policy, and the resulting volatility across equity markets.

Diversify’s Take:

The Path to De-Escalation:

Though this war clearly has many geopolitical considerations (Iran’s possession of 900 pounds of enriched uranium, unclear leadership succession, potential for ethnic fragmentation and a sharp civilian uprising), the most important pressure point is how the Strait will be governed going forward. The U.S. and most nations want the Strait to remain a free maritime zone under international oversight. Iran wants sovereignty over the Strait with the right to transition it into a lucrative toll booth. The entire world is being held hostage from the Strait’s closure, so these negotiations carry enormous stakes. The global pressures are mounting. But the Strait question can't be resolved in isolation. Who governs Iran, and whether that government can credibly enforce any agreement, will determine whether an eventual deal sticks.

A common military maxim is that it takes one side to start a war but two to end it. On March 26th, the Trump administration announced a 10-day pause on military strikes on Iranian energy infrastructure, setting an April 6th deadline for Iran to re-open the Strait. On March 31st, President Trump said that the U.S. is “in serious discussions with a new and more reasonable regime.” On Tuesday, Iran said the country was ready to end the war if given guarantees against future aggression. Potential two-sided alignment sent global stocks soaring.

A short-term de-escalation is one thing; a lasting de-escalation is what our oil-dependent global economy needs, and that may be tougher to achieve. Some of the damage has already been done, and supply chain disruptions compound further each week that passes. There may be long-term repercussions for the region that persist beyond any ceasefire. Though we’re optimistic that U.S./Iran channels of communication may be opening, the fog of war remains, and we expect several twists and turns ahead. It wouldn’t surprise us to see on-again, off-again negotiations, a resolution to open the Strait followed by threats to reclose it, followed by ceasefire violations.

Our base case is that the economic costs of a prolonged Strait closure are too high and too far-reaching for both sides to sustain indefinitely. Iran’s economy is crumbling with each passing day. We’re confident there will eventually be a path to resolution, but it might be messy and non-linear.

Inflation’s Transmission Mechanism:

It was clear in early March that if the war persisted, high energy costs would begin to bleed into the price of other goods and services. That is starting to happen. The national average gas price is hitting $4.00 per gallon, and other energy prices like diesel and jet fuel have surged considerably more. Every good across the globe just became more expensive to transport, which lifts aggregate prices across the board.

Energy prices get the headlines, but the downstream effects from the Strait’s closure ripple through diverse industries. For example, the Gulf States are major suppliers of petrochemicals used in plastics and packaging, ammonia used in fertilizers, which impacts global food prices, and helium used in semiconductor manufacturing. An oil shock doesn't stay at the pump. With enough time, it feeds into grocery stores, factory floors, and chip fabs, resulting in widespread margin implications for companies and pinched budgets for consumers.

Inflation expectations have moved accordingly. The OECD raised its U.S. 2026 headline inflation forecast from 2.8% to 4.2%. Core CPI, which strips out food and energy, will likely jump back into the 3% range. The April 10th CPI print will be the first real datapoint of whether the Strait's closure is bleeding into non-energy inflation.

The path of inflation will be determined by the duration of the war. So, time is of the essence. Even if a ceasefire is declared in the near term, it may take several months for global energy availability to return to pre-war levels, and some of the destroyed LNG facilities may take years to rebuild. Encouragingly, the oil futures curve remains in deep backwardation, meaning contracts further out are trading well below spot prices. The forward curve has WTI and Brent at $71 and $78 per barrel by December 2026, respectively. Those curves are consistent with the view that there will be some form of resolution leading to tankers flowing through the Strait again within weeks or months. But if months become quarters, inflation has room to run further than most expect.

Direction of Global Monetary Policy:

If inflationary pressures continue to build, the question becomes: what can central banks do about it? If the Fed raises rates to fight energy-driven inflation, it risks slamming the brakes on the economy already showing geopolitical-induced vulnerability and labor market weakness. If the Fed holds or cuts to support growth, it risks inflation expectations drifting higher and becoming entrenched. The core question is whether this energy shock is transitory. We’ve heard that word before.

Before the conflict broke out, the rates market priced in an 80% chance that the Fed would cut rates twice by year-end. Those odds have dropped to 3%, with a 22% probability of one cut by year-end. On March 5th, we noted that one cut had already been priced out. Now, the rates market’s view is that the current policy rate of 3.50-3.75% will hold steady all year. With so many moving parts, including the probable but not certain odds that Fed Chair nominee Kevin Warsh will take the FOMC reins from Chair Powell in May, we think the Fed stays put.

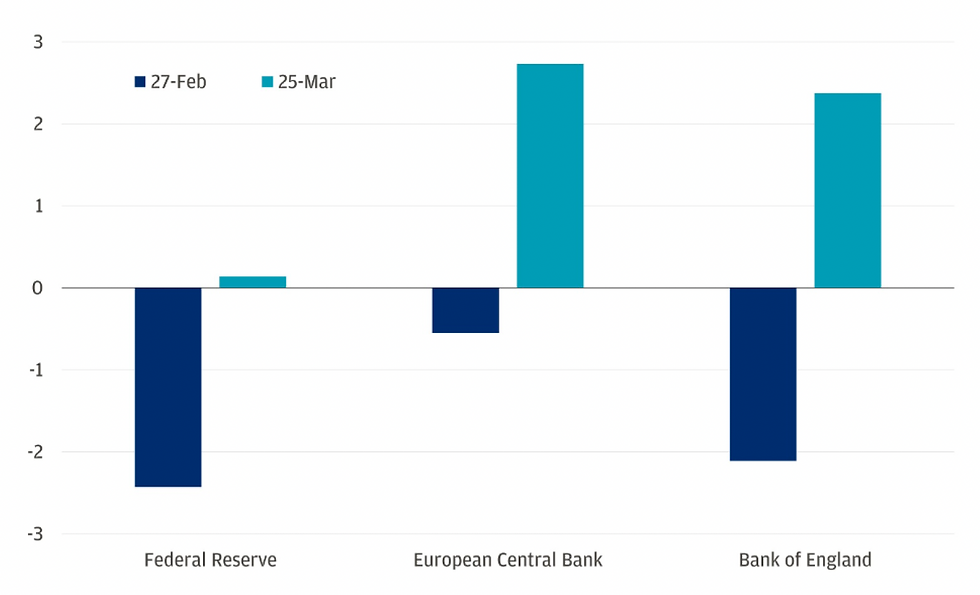

This is not just a U.S. story. In March, the ECB held its rate at 2.0%. Its cutting cycle, which has been in place since June 2024, is now frozen, and markets are pricing in 75bps of ECB hikes by year-end. The Bank of England also held its rate at 3.75% after being on the verge of cutting before the war began. The chart below from J.P. Morgan shows the shift in the market's year-end 2026 rate path expectations from February to March for three of the world's most important central banks.¹

Investment Implications:

Fixed Income:

The rates discussion above matters because short-term rates sit at the epicenter of the capital markets, and they just went up. Short rates are the base on which intermediate- and long-term yields are established, the level to which credit spreads are added. Collectively, yields are the discount mechanism for every other asset class: equity, commercial real estate, and anything whose value is derived from discounting future cash flows to arrive at a present value.

Bonds often serve as a valuable portfolio tool during geopolitical shocks. But because this episode’s energy shock is resetting near-term inflation expectations, bonds have generally drifted lower over the last month. The correlation between stocks and bonds turned positive in March, meaning both asset classes moved in the same general direction. The 10-Year Treasury yield touched 4.47% before retreating to 4.31% where it stands today. Broad U.S. bonds are roughly flat YTD.

We’ve deliberately maintained shorter-than-benchmark duration in our bond portfolios given our views on inflation. With the exception of municipal bonds, most bond segments aren’t offering adequate compensation to take on excessive duration risk. We continue to favor direct ownership of high-quality laddered bonds that match maturities with planned cash flows. Despite the rise in yields, bonds are broadly outperforming stocks YTD, reinforcing the importance of maintaining strategic fixed income allocations in diversified portfolios.

Equity:

On March 31st, the S&P 500 surged +2.9% on hopes of a de-escalation, earning a spot on the top 10 list of largest single-day gains over the last decade. Market history informs us that the best days often cluster tightly around the worst ones, when fear is at its peak.

That surge was a stark reminder of the importance of maintaining a long-term investment orientation, despite the behavioral temptation to sell during periods of acute stress. A continuous investment in the S&P 500 over the last 20 years has earned a +9.0% annualized return. Over that period, if you missed just the top 10 best days, your return would have been cut in half to +4.6%.²

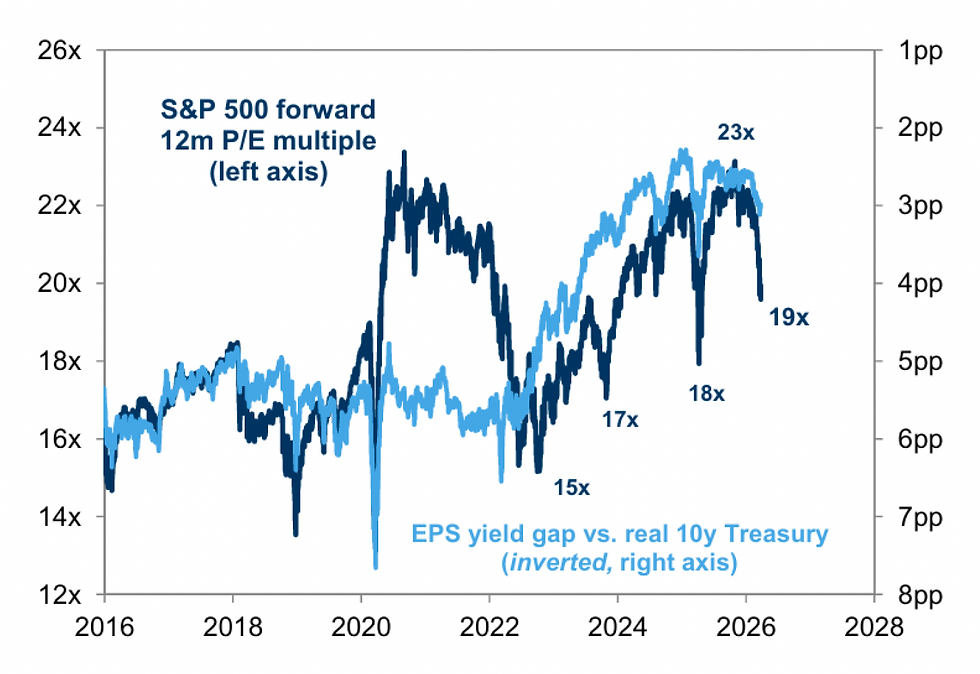

According to Mike Wilson, Morgan Stanley’s Chief U.S. Equity Strategist, more than half of the Russell 3000 stocks are down at least 20% from their prior highs. From a valuation perspective, global stock multiples have compressed 5-15% over the last month. As the Goldman Sachs chart below shows, the S&P 500’s forward P/E just went from the October 2025 high of 23x to 19x today.³ A reset of expectations is healthy and beneficial for future returns.

We believe quality matters more than ever in this environment. Pricing power, in particular, is paramount when margin compression may be on the horizon. Companies that can pass through higher input costs will separate from those that cannot. The broadening of market leadership we've highlighted continues its recent trend: value is leading growth, equal-weight is leading cap-weight, international is leading U.S. In a market with this wide a range of outcomes, diversification is not just a principle; it is a measurable advantage.

Summary:

The Iran conflict has evolved from a geopolitical shock into a meaningful global economic event. Oil above $100, rising inflation expectations, a frozen Fed, and compressed equity multiples describe the current environment. Our base case remains that the economic costs of a prolonged Strait closure will force both sides to the table, but the path to resolution won’t be smooth.

The less visible the road ahead, the more risk management matters. This is where Diversify Advisors add incredible value, ensuring that your asset allocation across cash, bonds, stocks, and private market investments is dialed in, personally tailored to your financial picture, and well-constructed for a wide range of outcomes. We are positioning for a world where inflation runs hotter than expected, rates stay higher for longer, and pricing power separates winners from losers. Quality, diversification, and shorter duration remain central to how we’re positioned. We're watching this closely and will be back with updates as conditions change.

David Wrigley

Chief Investment Officer

J.P. Morgan Asset Management, as of March 25, 2026

Bloomberg, S&P Dow Jones Indices, as of December 31, 2025

Goldman Sachs Global Investment Research, as of March 27, 2026

The information contained herein is the opinion of the author as of the date the market update was written and is subject to change without notice as markets change, and new information is available. While Diversify utilizes sources deemed to be reliable, we have not independently verified the content. Investors should carefully consider any changes based on this market commentary and discuss their individual circumstances with their trusted advisors. Past performance is not indicative of future results. This communication is for informational purposes only and should not be construed as investment advice or a recommendation.